Finding the right lender for a commercial real estate deal or small business loan has traditionally meant weeks of cold calls, inconsistent information, and stacks of paperwork submitted to lenders who may not even fit your profile. That friction costs investors and business owners time they cannot afford to lose. Real-time lender matching changes the equation entirely. This guide explains how the technology works, why it outperforms traditional loan searches, and how real estate investors and small business owners can use it to access capital faster and with greater precision than ever before.

Table of Contents

- Understanding real-time lender matching

- How real-time lender matching works: Behind the scenes

- Comparing real-time lender matching with traditional loan searches

- Who benefits from real-time lender matching?

- Rethinking access to capital: Why automation matters more than ever

- Explore your options with CR Equity AI

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| AI powers faster matches | Real-time lender matching uses advanced AI to connect borrowers and lenders in seconds based on dozens of data points. |

| Better fit loans | Automated systems only show you matched lenders whose criteria fit your needs, saving time and reducing rejections. |

| Ideal for investors and small businesses | These platforms deliver maximum benefit to real estate investors and business owners seeking quick, efficient access to credit. |

| Compare with confidence | Real-time matching enables you to see and choose from best-fit loan offers instantly—no more manual searching. |

Understanding real-time lender matching

Real-time lender matching is the automated process of connecting borrowers to lenders using advanced algorithms and artificial intelligence (AI). Rather than requiring borrowers to manually research lenders, submit multiple applications, and wait for responses, the system evaluates a borrower's financial profile and instantly identifies lenders whose criteria align with that profile.

The concept is straightforward, but the technology behind it is sophisticated. AI underwriting in commercial real estate has evolved to the point where machines can assess risk, evaluate creditworthiness, and route loan requests more accurately than a human loan officer reviewing a single file. The platform pulls data from multiple sources, processes it simultaneously, and delivers ranked lender matches within seconds.

Key data points that drive the matching process include:

| Data Category | Examples |

|---|---|

| Borrower financials | Revenue, credit score, debt-to-income ratio |

| Loan characteristics | Loan type, loan amount, loan-to-value ratio |

| Business profile | Industry, years in operation, entity type |

| Geographic factors | State, market type, property location |

| Lender criteria | Interest rate range, minimum DSCR, timeline |

These inputs are evaluated simultaneously against a curated database of lenders. AI systems evaluate 50+ borrower data points including revenue, credit score, and industry, routing each application by variables such as geography, loan amount, and lender-specific requirements. The result is a shortlist of lenders who are genuinely likely to approve the loan, not just a generic directory of options.

"Lender matching methodologies use AI to evaluate 50+ borrower data points against lender criteria, routing applications by variables like credit score, geography, and loan amount to surface the most relevant capital sources in real time."

This level of precision matters because lender requirements vary significantly. A lender focused on self-storage acquisitions in the Sun Belt operates with entirely different underwriting standards than a community bank offering SBA loans in the Midwest. Matching borrowers to the right lender type reduces wasted applications, protects credit scores from unnecessary inquiries, and increases the probability of approval on the first submission.

For real estate investors, this means faster deal closings and fewer missed opportunities due to capital delays. For small business owners, it means access to a broader pool of lenders without the burden of individually researching each one. The efficiency gain is not marginal. It is structural.

How real-time lender matching works: Behind the scenes

After understanding what lender matching is, it is helpful to look behind the scenes at how this process actually works from input to funded loan.

The process follows a clear sequence:

- User inputs: The borrower submits basic financial and loan information through a digital intake form. This includes credit score, annual revenue, loan amount requested, loan purpose, and location.

- Data aggregation: The platform pulls additional data from connected sources, including bank statements, tax records, and public property data, to build a complete borrower profile.

- AI decisioning: Machine learning models evaluate the borrower's profile against a database of active lenders, scoring each lender match based on fit, approval likelihood, and terms alignment.

- Real-time matching: The system routes the application to the highest-scoring lenders simultaneously, generating multiple offers or expressions of interest within minutes.

- Outcome delivery: The borrower receives a ranked list of lender offers with key terms, allowing direct comparison without submitting separate applications to each lender.

Understanding how AI underwriting works clarifies why this process is so much faster than traditional methods. The AI does not need to review documents sequentially. It processes all variables in parallel, which compresses what used to take weeks into a matter of seconds.

Consider a practical example. A small business owner needs a $200,000 working capital loan. She has a 680 credit score, three years in operation, and $850,000 in annual revenue. In a traditional process, she might spend two weeks identifying potential lenders, submitting applications, and waiting for responses, only to discover that several lenders require a minimum of five years in business. With real-time matching, the AI filters out those lenders immediately and surfaces only the options for which she qualifies. She receives three competitive offers within minutes.

The variables that drive this precision include both borrower data and lender criteria. On the borrower side, the system considers credit history, cash flow patterns, collateral, industry risk ratings, and geographic market conditions. On the lender side, it accounts for minimum loan amounts, preferred asset classes, maximum loan-to-value ratios, and required debt service coverage ratios (DSCR). DSCR measures a property's ability to cover its debt payments from operating income, and many commercial lenders set a minimum threshold, often 1.20 or higher.

Pro Tip: Keep your financial records current and organized before entering a matching platform. Accurate revenue figures, up-to-date tax returns, and a clean credit profile increase your match score and improve the quality of offers you receive.

Comparing real-time lender matching with traditional loan searches

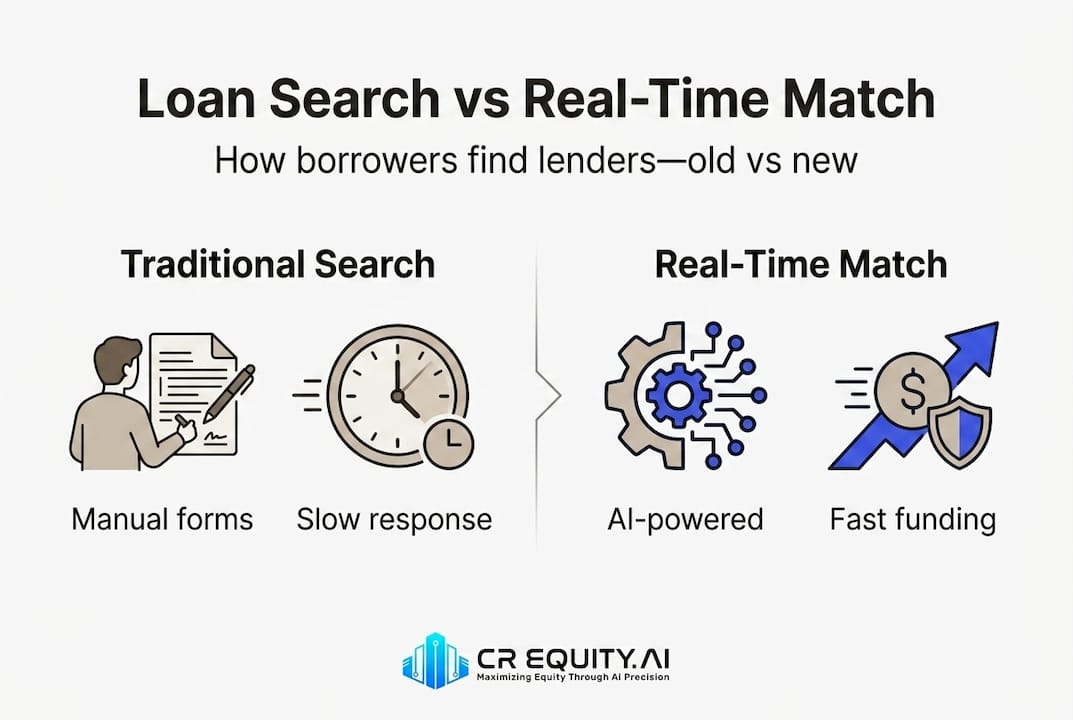

Having seen the technology, it is important to weigh how real-time lender matching stacks up against the conventional loan search process.

Traditional loan searches involve a borrower independently identifying potential lenders, often through referrals or internet research. Each lender then requires a separate application, often with its own document checklist. The borrower submits materials, waits for an underwriter to review the file, and then receives a decision, sometimes weeks later. If that lender declines, the process restarts with the next candidate.

The contrast is significant:

| Factor | Traditional search | Real-time matching |

|---|---|---|

| Time to first offer | 1 to 4 weeks | Minutes |

| Number of applications required | One per lender | Single intake form |

| Match quality | Inconsistent | Algorithm-optimized |

| Lender pool size | Limited by network | Platform-wide database |

| Credit inquiry impact | Multiple hard pulls | Typically one soft pull |

| Transparency | Low | High, with side-by-side terms |

The AI evaluation of 50+ data points per borrower means the matching process surfaces lenders with far greater accuracy than a borrower could achieve through manual research alone. The speed advantage alone is transformative for time-sensitive deals.

Common pitfalls in traditional loan searches include:

- Missed matches: Borrowers often overlook lenders outside their immediate network, missing better rates or more flexible terms.

- Wasted paperwork: Submitting full applications to lenders who ultimately do not fit the borrower's profile wastes time and resources on both sides.

- Slower speed: Weeks-long timelines can cause real estate investors to lose deals to faster-moving buyers with pre-arranged capital.

- Inconsistent information: Different lenders present terms in different formats, making apples-to-apples comparisons difficult without a standardized platform.

- Credit score damage: Multiple hard inquiries from separate lender applications can lower a borrower's credit score during the search process.

Understanding the difference between a bridge loan vs traditional loan further illustrates why lender fit matters. Bridge loans require lenders with specific risk appetites and short-duration underwriting expertise. A traditional bank search rarely surfaces the right bridge lender quickly. Automated matching platforms maintain curated databases of specialty lenders, including those focused on bridge, construction, and non-QM (non-qualified mortgage) products.

The future of business lending is clearly moving toward automation. Borrowers who continue relying on manual searches face a structural disadvantage in both speed and match quality compared to those using AI-powered platforms.

Who benefits from real-time lender matching?

With the comparison in mind, it is worth focusing on who truly stands to gain from adopting real-time lender matching.

Real estate investors are among the primary beneficiaries. Acquisition timelines in commercial real estate are often compressed, particularly in competitive markets. An investor pursuing a self-storage facility, a multifamily property, or an industrial asset needs capital commitments quickly. Real-time matching surfaces bridge lenders, DSCR lenders, and commercial mortgage options that align with the specific asset class and deal structure, without weeks of outreach. Investors can compare multiple term sheets simultaneously and move to the due diligence phase faster.

Small business owners gain access to a lender pool that would otherwise require significant time and connections to reach. Many small business owners lack relationships with specialty lenders or private credit funds. Real-time matching removes that barrier. The AI matching methodology evaluates each borrower's revenue, credit score, and industry against lender requirements, ensuring that only relevant offers are returned. This reduces rejection rates and improves the overall borrowing experience.

Other groups that benefit significantly include:

- Startups and early-stage companies that fall outside traditional bank lending criteria but qualify for alternative or asset-based financing.

- Franchise operators seeking equipment financing or working capital with specific lender requirements tied to franchise brand approval.

- Non-traditional credit borrowers including self-employed individuals and foreign nationals who need non-QM or DSCR-based loan products.

- Brokers and intermediaries who use matching platforms to source the right capital for multiple clients simultaneously, improving their own efficiency and client outcomes.

Top advantages for real estate investors and small business owners specifically:

- Receive multiple, pre-qualified offers from a single application submission.

- Compare loan terms, rates, and timelines side by side without additional paperwork.

- Access specialty lenders, including bridge, construction, and non-QM providers, not typically found through general searches.

- Reduce time from application to funding commitment, often from weeks to days.

The future of commercial real estate increasingly favors investors who can move fast and close with certainty. Real-time lender matching is one of the clearest tools available to achieve that advantage.

Pro Tip: Use platforms that allow you to compare multiple lender offers without triggering additional credit applications for each one. This protects your credit score while maximizing your visibility into available terms.

Rethinking access to capital: Why automation matters more than ever

The conventional advice given to borrowers for decades has been to shop widely, build lender relationships, and rely on your network. That advice was reasonable when information was scarce and lender databases were not accessible. It is largely outdated now.

Automated lender matching does not just replicate the manual process faster. It fundamentally changes which lenders a borrower can access. A real estate investor in a secondary market with no existing lender relationships can now surface institutional-grade capital sources that previously required a broker or an introduction. The playing field is more level than it has ever been.

There is also a persistent myth that AI-driven systems favor large borrowers or institutional profiles. In practice, well-designed matching algorithms prioritize borrower-lender fit above loan size. A $150,000 business loan and a $5 million commercial acquisition can both be matched accurately when the underlying data is complete and the lender database is sufficiently broad.

The future of business lending belongs to borrowers who treat technology as a primary tool rather than a secondary option. Waiting for a relationship banker to return a call while a deal window closes is a choice, not a necessity. Real-time matching puts the borrower in control of the process from the first moment of inquiry.

Explore your options with CR Equity AI

Ready to experience real-time lender matching for yourself? CR Equity AI combines machine learning underwriting, automated document intelligence, and a curated lender network to deliver multiple offers in minutes, not weeks.

Whether you are a real estate investor seeking bridge or construction financing or a small business owner looking for working capital, CR Equity AI's AI-driven credit infrastructure is built to match your profile to the right capital source with institutional-grade accuracy. Use the loan calculator to estimate your financing options, or explore the full range of commercial real estate loan services available on the platform. Faster decisions, transparent terms, and scalable capital start here.

Frequently asked questions

How does real-time lender matching determine the right lender for me?

AI algorithms analyze over 50 variables, including your credit score, revenue, industry, and loan amount, matching your profile to lender criteria for optimal loan offers in seconds.

Can real-time lender matching improve my chances of getting approved?

Yes, because you are only matched with lenders whose requirements closely align with your financial profile, as determined by AI-evaluated borrower data points and lender-specific criteria.

Is real-time lender matching only for large loans or commercial real estate?

No. The technology is used across a wide range of loan types, including bridge loans, business term loans, and smaller investment properties, as the matching methodology is designed to route by loan amount and product type regardless of deal size.

What information do I need to provide for real-time matching?

Typically, you will need your credit profile, business revenue, requested loan amount, loan purpose, and sometimes your industry or geographic location, all of which feed the AI's borrower evaluation process.

Recommended

- Fast, Direct Lending You Can Trust at CR Equity | CR Equity AI

- Fast Business Funding & Business Loan Fast Approval | AI Business Loan | CR Equity AI | CR Equity AI

- Flex 50™ | Fast Commercial Bridge Loan & CRE Refinance | 24–48 Hour Funding | CR Equity AI

- How to Get a Commercial Real Estate Loan in 3 Days | CR Equity AI | CR Equity AI