7 min read

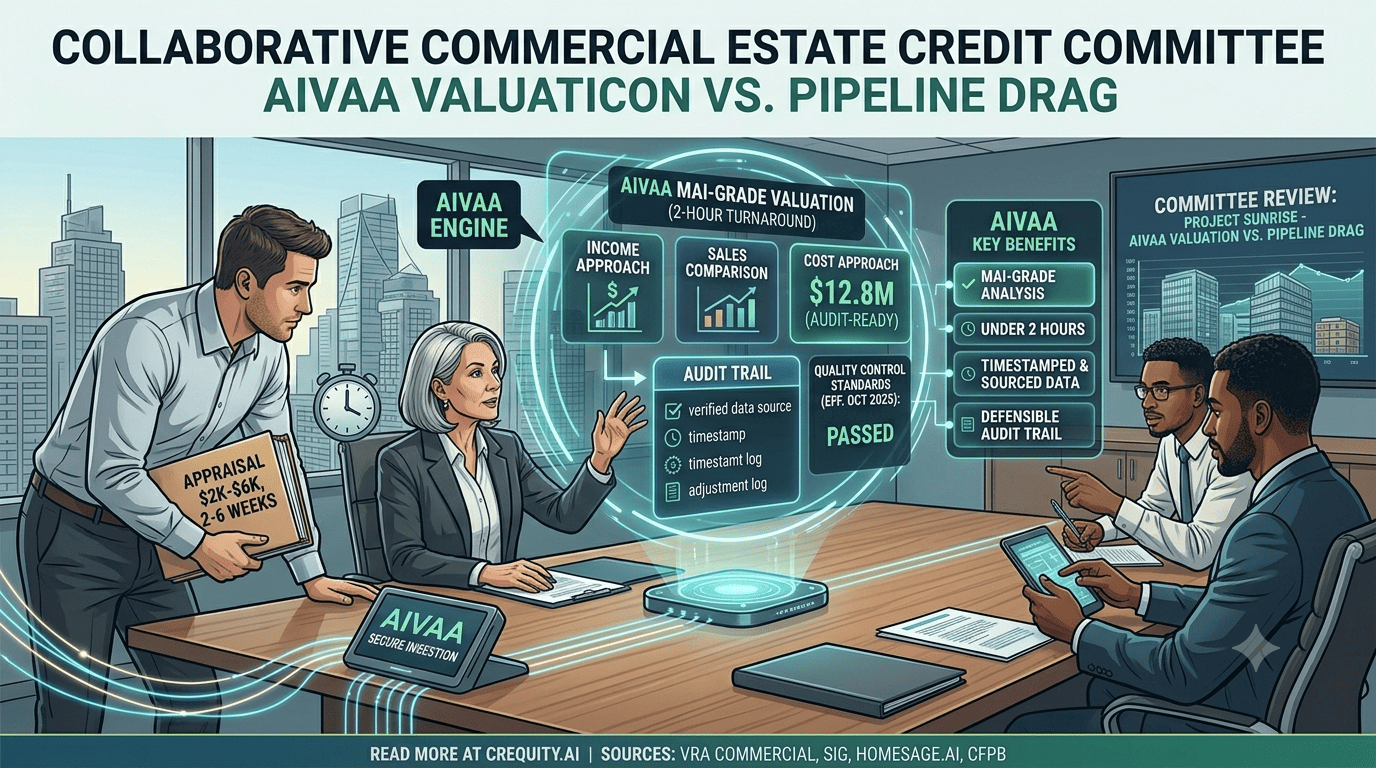

A traditional commercial appraisal is a slow, expensive necessity. Industry pricing guides put a typical commercial appraisal at roughly $2,000 to $6,000, with turnaround commonly running two to six weeks depending on complexity and data availability. For a single asset that is an inconvenience. Across a pipeline, it is a structural drag on how fast capital can move.

The AIVAA engine was built to remove that drag without removing the rigor. It produces an MAI-grade valuation in under two hours — and, just as importantly, one that a lender, an auditor, or a credit committee can defend line by line. The goal was never to cut corners. It was to deliver appraisal-quality analysis at a fraction of the time and cost, with a stronger audit trail than the manual process it replaces.

What the AIVAA engine actually does

AIVAA — the AI Valuation and Analysis engine — does not replace appraisal judgment. It operationalizes it at machine speed. The engine ingests property characteristics, income data, market comparables, and macro inputs, then applies the same three approaches a credentialed appraiser uses: income, sales comparison, and cost.

The difference is throughput and consistency. The engine applies the methodology identically on every asset, every time, without fatigue or the anchoring bias that creeps into manual review — and it shows its work at each step. A human appraiser closing two or three assignments a week is constrained by hours in the day; a methodology encoded in software is not.

Why the data and the audit trail are the whole point

A valuation is only as defensible as the data behind it. AIVAA draws on verified property data, recorded transactions, rent and expense benchmarks, and current market conditions. Every input is timestamped and sourced, and every adjustment is logged.

That audit trail is what makes the output defensible. When a credit committee or a regulator asks how a number was reached, the answer is a complete, reconstructable record — not an analyst’s recollection of a spreadsheet from three weeks ago. In a world where valuation methodology is under closer scrutiny than ever, the ability to reproduce a number on demand is becoming a requirement rather than a feature.

Automated valuation is already mainstream — and now regulated

Skeptics sometimes treat algorithmic valuation as experimental. The lending market has moved past that. According to the Mortgage Bankers Association’s 2025 Home Equity Lending Study, 47% of home equity and HELOC originations in 2024 were subject to an automated valuation model — the highest share on record and more than double the level seen at the start of the decade.

Regulation has caught up in step. U.S. financial regulators finalized interagency AVM quality-control standards, effective October 2025, requiring documented accuracy testing, bias safeguards, and conflict-of-interest controls for models used in lending. For institutional users, that is a positive: it draws a clear line between enterprise-grade valuation systems with documented validation and consumer-facing estimate tools. Defensible automation is exactly what the rules now demand.

How lenders actually use a two-hour valuation

For a lender, the value of speed is really speed plus confidence. A two-hour valuation means a loan officer can put an indicative number on the first call instead of the second week. A standardized methodology means the credit committee is comparing assets on a like-for-like basis across the entire portfolio rather than reconciling the styles of a dozen different appraisers.

And because the output is audit-ready, the valuation holds up across the loan’s full lifecycle — origination, servicing, and any eventual securitization or sale. The number does not have to be rebuilt every time it is questioned; it can simply be reproduced. For an institution measuring itself on funding speed, that is the difference between a quote that takes hours and one that takes weeks.

Where human judgment still leads

Honesty about the limits is part of what makes the system credible. Low-confidence outputs — unusual property types, thin comparable sets, distressed or special-use assets — are a signal to escalate to a hybrid or full appraisal, not a green light to proceed on the model alone. The engine’s job is to handle the volume that is genuinely routine at speed, and to flag clearly the cases that warrant a credentialed human. That division of labor is what makes the output trustworthy.

Key takeaways

-

Traditional commercial appraisals run ~$2,000–$6,000 and 2–6 weeks — a structural drag across a pipeline.

-

AIVAA delivers MAI-grade valuation in under two hours by applying the income, sales-comparison, and cost approaches identically every time.

-

Every input is timestamped and sourced, so a valuation can be reconstructed on demand for a credit committee or regulator.

-

AVMs are already mainstream — 47% of 2024 home-equity originations used one (MBA) — and now sit under finalized federal quality-control standards (effective Oct 2025).

-

Low-confidence cases are flagged for human escalation, not pushed through — the engine handles routine volume and defers on genuine complexity.

Appraisal-quality analysis no longer has to mean appraisal-length timelines. To see how the AIVAA engine values your next asset in under two hours — with an audit trail your credit committee can stand behind — request a walkthrough at crequity.ai or contact the team at support@crequity.ai.

Sources

-

VRA Commercial — Why a Commercial Appraisal Costs More (cost & timeline ranges) — https://www.vracommercial.com/article/why-does-a-commercial-appraisal-cost-more-than-a-residential-appraisal/

-

SIG — Commercial Real Estate Appraisal: What You Need to Know (2–6 week timeline) — https://sandsig.com/news/commercial-real-estate-appraisal-what-you-need-to-know/

-

Homesage.ai — Enterprise Guide to Automated Property Valuation Systems for Lenders 2026 (MBA AVM stat, CFPB rule) — https://homesage.ai/resources/blog/guide-automated-property-valuation-systems-for-lenders-2026/

-

CFPB — Interagency Automated Valuation Models Final Rule — https://files.consumerfinance.gov/f/documents/cfpb_automated-valuation-models_final-rule_2024-06.pdf