How AI streamlines funding for real estate and business growth

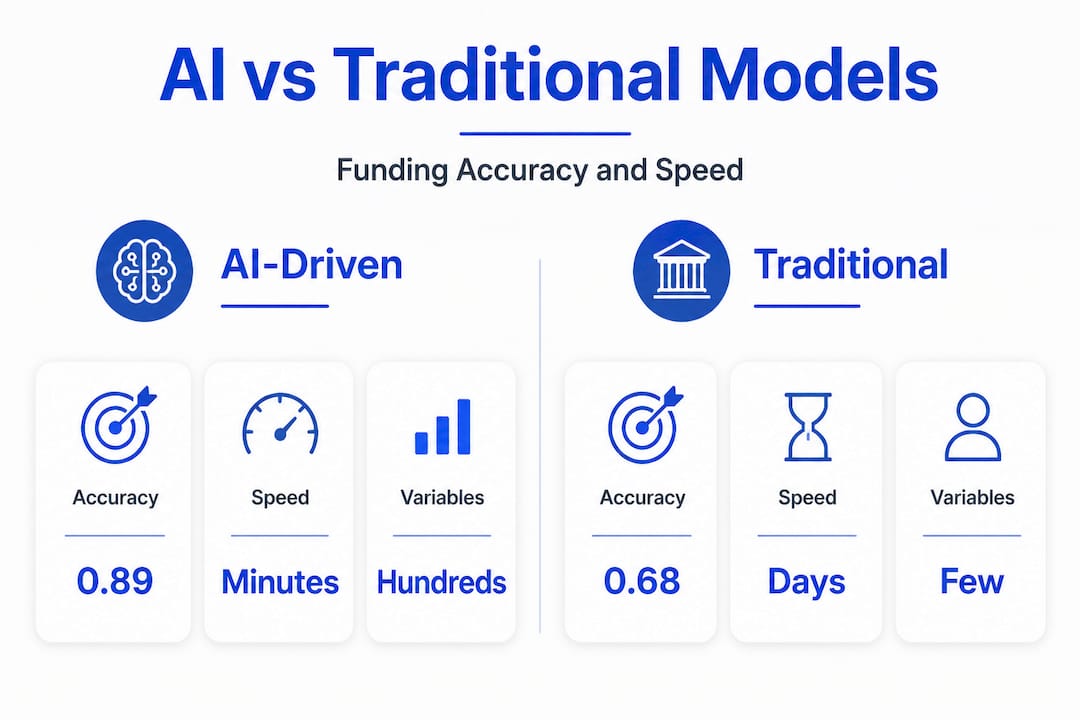

AI-powered credit models are now outperforming traditional underwriting in both speed and accuracy, and that shift is changing who gets funded and how fast. Machine learning models like XGBoost achieve an AUC of 0.89 versus 0.76 for traditional logistic regression, with stronger stress-test stability at 0.83 versus 0.68. For real estate investors and business owners, this is not a theoretical upgrade. It is a measurable change in deal speed, approval rates, and access to capital. This article breaks down how AI transforms the full funding lifecycle, what technology drives the results, and how you can position yourself to benefit right now.

Table of Contents

- Why traditional funding holds you back

- How AI accelerates and improves funding decisions

- AI vs. traditional credit models: How do they stack up?

- Pitfalls, bias, and regulatory hurdles: What to watch out for

- Putting AI-powered funding to work: What investors and businesses can do today

- What most investors miss about AI in funding: A reality check

- Accelerate your next deal with AI-powered funding

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| AI speeds loan approvals | AI models quickly analyze credit and risk, cutting approval times from days to hours. |

| Greater inclusion and accuracy | AI expands funding access while outperforming traditional scoring in stability and defaults. |

| Limitations demand oversight | AI can introduce bias and struggles with outliers, so human review and transparency remain essential. |

| Hybrid models work best | Combining human and AI strengths delivers reliable, ethical, and scalable lending decisions. |

| Investors have actionable steps | By vetting AI platforms and asking the right questions, you can safely benefit from smarter funding solutions. |

Why traditional funding holds you back

Conventional underwriting was built for a slower era. Loan officers review stacks of documents manually, verify income through paper trails, and rely heavily on personal relationships and subjective judgment. The result is a process that takes weeks, not hours, and often excludes creditworthy borrowers simply because their financial profiles do not fit a rigid template.

The core bottlenecks include:

- Document-heavy workflows that require repeated submissions of tax returns, bank statements, and entity agreements

- Geographic constraints that favor borrowers near major financial centers over those in rural or underserved markets

- Soft information dependency, where lender relationships and local reputation influence decisions more than objective data

- Opaque risk assessments that make it difficult for borrowers to understand rejections or improve their applications

- High cost of exceptions, where non-standard deals require senior credit officer review, adding days or weeks to timelines

The bias problem is especially significant. Traditional models rely on FICO scores, W-2 income, and established banking relationships. This systematically disadvantages self-employed borrowers, small business owners with variable revenue, and investors operating in secondary markets.

Research shows that banks using AI lend more to distant small business borrowers, especially in poorer areas, with lower default rates and interest spreads, and reduced reliance on soft information.

That finding matters. It means the traditional system was not just slow. It was structurally excluding viable borrowers. Understanding the future of business lending requires acknowledging that the old model’s flaws were baked in, not incidental.

How AI accelerates and improves funding decisions

AI does not just speed up the same process. It fundamentally changes the inputs, the analysis, and the outputs of credit decisions.

Traditional models analyze a handful of variables: credit score, debt-to-income ratio, loan-to-value, and employment history. Machine learning models analyze hundreds or thousands of variables simultaneously, including alternative data sources like utility payment history, rent payments, cash flow patterns, and real-time market data. This broader view produces more accurate risk assessments.

Here is how the performance stacks up:

| Model | AUC (Normal) | AUC (Stress Test) | Speed |

|---|---|---|---|

| XGBoost (ML) | 0.89 | 0.83 | Minutes |

| Neural Network | 0.87 | 0.81 | Minutes |

| Logistic Regression | 0.76 | 0.68 | Days |

The XGBoost superiority over traditional models is not marginal. The AUC gap at 0.89 versus 0.76 represents a meaningful difference in predictive accuracy, and that gap widens under economic stress.

Real-world outcomes confirm the data. In a study analyzing 4.5 million loans at a Chinese bank, AI combined with big data reduced unclassified credit ratings by 40.1% and loan defaults by 29.6%. These are not incremental improvements. They represent a structural upgrade in credit quality.

How AI delivers faster approvals in practice:

- Automated document ingestion extracts and verifies data from financial statements, tax returns, and entity documents without manual data entry

- Real-time risk scoring runs multiple models simultaneously and returns a risk profile in seconds

- Lender matching algorithms identify the optimal capital source for each deal based on risk appetite, loan type, and geography

- Automated KYC/AML checks clear compliance requirements digitally, eliminating days of back-and-forth

- Offer optimization engines present borrowers with multiple term structures ranked by cost and fit

Pro Tip: When evaluating AI-driven lenders, ask specifically whether their models are retrained on recent data. A model trained on pre-2020 loan performance may underweight post-pandemic credit dynamics, which affects accuracy in today’s market.

The AI underwriting revolution in commercial real estate is particularly relevant for investors structuring bridge loans, construction financing, and self-storage acquisitions, where speed and certainty of execution are competitive advantages. Understanding how AI underwriting works at the technical level helps borrowers and investors engage more effectively with lender platforms. The challenge, as AI in regulated finance requires, is balancing model complexity with regulatory explainability.

AI vs. traditional credit models: How do they stack up?

The performance difference between AI-driven and traditional credit scoring is significant, but the practical implications vary by deal type, borrower profile, and lender sophistication.

| Feature | AI-Driven Models | Traditional Models |

|---|---|---|

| Predictive accuracy (AUC) | 0.87 to 0.89 | 0.68 to 0.76 |

| Data inputs | Hundreds of variables | 5 to 15 variables |

| Processing speed | Minutes to hours | Days to weeks |

| Alternative data use | Yes (cash flow, rent, utilities) | Limited or none |

| Geographic reach | Broad, including rural markets | Concentrated in primary markets |

| Explainability | Requires engineered solutions | Built-in (human readable) |

| Stress test stability | High (AUC 0.83) | Lower (AUC 0.68) |

The XGBoost vs. logistic regression performance gap highlights a critical trade-off: AI models are more accurate but less inherently transparent. This creates a real challenge for regulated lenders who must explain adverse action decisions to borrowers.

For real estate investors, AI-driven platforms offer a concrete edge in acquisition timing. When a bridge loan needs to close in 10 days, waiting three weeks for a traditional underwriting decision is not a viable option. AI platforms can return a term sheet in hours, enabling faster contract execution and competitive positioning.

When to rely on AI:

- Straightforward deals with clean financials and standard collateral

- Portfolio lenders with established AI credit frameworks

- High-volume decisions where pattern recognition adds accuracy

- Borrowers with non-traditional income who would score poorly under FICO-only models

When human review matters:

- Complex entity structures with multiple guarantors

- Properties with environmental concerns or title complications

- Borrowers recovering from situational credit events (divorce, medical, business disruption)

- Loan structures requiring covenant customization

Pro Tip: Platforms offering hybrid models, where AI handles the initial scoring and a senior credit officer reviews edge cases, deliver the best of both worlds. This structure reduces approval time while protecting against model errors on non-standard deals. AI-driven valuation tools work similarly, combining algorithmic speed with expert validation for defensible outcomes. For investors also evaluating traditional credit scoring for rentals, understanding how these benchmarks compare to AI-generated scores is increasingly important.

Pitfalls, bias, and regulatory hurdles: What to watch out for

AI-powered credit is not without risk. The same complexity that makes machine learning models more accurate also creates new categories of failure, and informed investors and borrowers need to understand them.

Key edge cases and limitations:

- Non-standard income sources: Gig workers, freelancers, and short-term rental operators often present income patterns that AI models trained on W-2 data do not interpret accurately

- Model drift: As economic conditions change, a model trained on historical data may produce increasingly inaccurate predictions without regular recalibration

- Bias amplification: If historical lending data reflects discriminatory patterns, AI models trained on that data can encode and scale those biases

- Explainability gaps: Regulators under the Equal Credit Opportunity Act (ECOA) require lenders to provide specific reasons for adverse credit decisions. Complex ensemble models can make this difficult to satisfy

Edge cases require human oversight: AI struggles with non-standard income, model drift, and bias from historical data, making explainable AI frameworks and audit trails essential for regulatory compliance.

The regulatory landscape is evolving rapidly. Lenders deploying AI in credit decisions face scrutiny from the Consumer Financial Protection Bureau (CFPB), the Federal Reserve, and state banking regulators. The concept of “glass-box AI” refers to model architectures designed to produce traceable, auditable decisions rather than black-box outputs that cannot be interrogated.

Pro Tip: Before engaging with any AI-driven lending platform, ask directly whether their models produce adverse action explanations that comply with ECOA and FCRA requirements. A platform that cannot answer clearly is a regulatory risk for both lender and borrower.

The future of commercial real estate is intertwined with AI adoption, but the most durable platforms will be those that prioritize compliance architecture alongside model performance. The regulatory tightrope for AI in regulated finance demands that speed never come at the expense of defensibility.

Putting AI-powered funding to work: What investors and businesses can do today

Knowing AI outperforms traditional models is useful context. Knowing how to act on that knowledge is what drives results. Here is a practical framework for selecting and engaging AI-driven lending platforms.

-

Identify platforms with documented AI frameworks. Ask lenders to describe their underwriting model architecture. Platforms using ensemble models (XGBoost, gradient boosting, neural networks) with regular recalibration are more reliable than those using AI as a marketing label for basic automation.

-

Evaluate transparency and adverse action processes. A responsible platform explains exactly why a loan was declined or structured a certain way. If a lender cannot provide specific, data-driven reasoning, their AI is either not functioning as advertised or not compliant.

-

Assess speed benchmarks with realistic deal timelines. The right question is not “how fast can you approve a loan?” but “how fast can you approve a loan for a deal with this specific profile?” Complexity affects speed, and a platform that cannot set realistic expectations will create execution risk.

-

Confirm regulatory compliance posture. Verify that the platform maintains audit trails, performs regular model audits, and can demonstrate ECOA-compliant adverse action notices. This protects you as a borrower in the event of disputes.

-

Look for hybrid human-AI models. Expert analysis confirms that hybrid models combining AI-driven pattern recognition with human judgment on exceptions and ethics outperform purely automated systems in both accuracy and risk management. The best platforms treat AI as a tool for senior credit professionals, not a replacement for them.

Pro Tip: Lenders are increasingly asking borrowers about their own AI adoption plans during underwriting. If you manage a portfolio or operate a business, documenting how you use data and technology in operations can strengthen your credit narrative on AI-native platforms.

Accessing fast, direct lending through an AI-driven platform requires preparation. Organize clean financial documentation, understand your DSCR metrics in advance, and be ready to explain any anomalies in your income or asset history before the platform’s model encounters them.

What most investors miss about AI in funding: A reality check

There is a tendency in the market to treat AI as either a silver bullet or a black box to be feared. Neither view is accurate, and both lead to poor decisions.

The more important truth is this: AI amplifies the quality of the inputs and the oversight structure around it. A well-designed platform with clean data, regular model audits, and experienced human oversight will outperform a traditional lender on speed, accuracy, and inclusion. A poorly designed platform with biased training data and no governance will systematically misclassify risk at scale.

Empirical evidence confirms superior accuracy, but concerns about black-box opacity, bias amplification, and regulatory explainability persist. Success hinges on glass-box AI with full traceability, not maximum model complexity.

For long-term investors, the question is not whether to use AI-driven lenders. It is whether the platforms you engage with have the governance infrastructure to make AI work reliably across market cycles. Model performance in 2021 looks very different from performance in 2023 or 2026. Platforms that do not account for economic regime changes in their model recalibration schedules introduce drift risk that compounds over time.

The investors who benefit most from AI-driven funding are those who understand how these models work, ask the right questions, and choose platforms that treat transparency as a structural feature rather than an afterthought. Exploring options like non-QM lending alongside AI-driven underwriting opens additional capital pathways for borrowers who fall outside conventional credit boxes.

Accelerate your next deal with AI-powered funding

Real estate investors and business owners working with traditional lenders are leaving speed, capital access, and competitive advantage on the table. The evidence is clear: AI-driven underwriting closes faster, serves more borrowers, and produces better credit outcomes at scale.

CR Equity AI delivers institutional-grade credit intelligence for real estate investors and business owners who need funding decisions in hours, not weeks. The platform combines machine-learning underwriting, automated document verification, and real-time lender matching to move your deal from application to term sheet faster than any traditional process. Whether you are financing a self-storage acquisition, a bridge loan, or a working-capital line, CR Equity AI has the infrastructure to match you with the right capital. Use the loan quote tool to model your deal terms, or explore how to invest in AI credit as a capital partner in next-generation lending.

Frequently asked questions

How does AI reduce funding approval times?

AI automates data analysis and decision-making across hundreds of variables simultaneously, which means loan approvals can happen in hours instead of days. AI combined with big data reduces unclassified credit ratings by 40.1% and loan defaults by 29.6%, demonstrating how much faster and more accurate automated analysis performs versus manual review.

Are AI-driven lending models fairer than traditional methods?

Empirical evidence shows AI can increase access and inclusion, but concerns about bias and explainability remain active areas of debate. Banks using AI lend more to distant small business borrowers in underserved areas with lower default rates, suggesting broader inclusion when models are well-designed.

What are the main risks or limitations of using AI for credit decisions?

AI can struggle with non-traditional income sources, model drift over time, and potential bias embedded in historical training data, so oversight and transparency are crucial. Regulatory compliance requires explainable AI frameworks and audit trails to satisfy ECOA and FCRA requirements.

How can investors evaluate if a lending platform uses responsible AI?

Look for clear adverse action explanations, hybrid human-AI review systems, regular model recalibration documentation, and platforms with strong compliance and audit trails built into their architecture.

Can AI-powered lending help underserved or remote businesses?

Yes. Research consistently shows that AI reduces geographic barriers for small business borrowers in poorer and more distant markets, expanding capital access while maintaining lower default rates than traditional lending in those same areas.

Recommended

- AI Commercial Real Estate Lending | Fast CRE Bridge & Business Loans | CR Equity AI

- The Future of Business Lending Is Here — And It’s Powered by AI | CR Equity AI

- The Future of Commercial Real Estate Transactions: Transforming Client Engagement with CR Equity.ai’s Ai Assistant | CR Equity AI

- Fast, Direct Lending You Can Trust at CR Equity | CR Equity AI