AI is originating credit and investment opportunities faster than the capital markets can fund them. The structural fix isn’t a bigger balance sheet — it’s a stack of off-take agreements. Here’s the data, and here’s how CR Equity AI is positioned to capture it.

In April 2026, Upstart Holdings (NASDAQ: UPST) did something that should have made every operator in AI-driven finance pay attention: it locked in a $1.25 billion forward-flow agreement with Fortress Investment Group — institutional capital committed, in advance, to buy up to 15 months of loans the company’s AI engine had not yet originated.1 It was the third such deal in a single spring.

Stacked against earlier commitments from Centerbridge Partners and a consortium of Eltura Ventures and Aperture Investors, institutional buyers have pre-committed more than $3.4 billion to absorb Upstart-originated credit.2 The company’s Q1 2026 revenue grew 44% year over year to $308 million — even as the stock traded roughly 67% below its 52-week high.3 The growth engine was never the problem. The funding structure was. And the market is only beginning to price what solving it is worth.

01 / THE GAP

AI is outpacing the capital markets

The defining constraint in AI finance is no longer model quality — it’s capital throughput. An AI underwriting engine can identify, structure, and price far more qualified opportunities than any single balance sheet, or any single equity raise, can fund. Left unsolved, that mismatch caps growth and strands pipeline.

The macro data makes the squeeze concrete. The top five US hyperscalers alone are projected to spend roughly $600 billion in capex in 2026 — a 38% jump over 2025 — overwhelmingly to build out AI infrastructure.4 Capital markets, not corporate balance sheets, are increasingly expected to fund that buildout, with debt playing a leading role, per Bloomberg data compiled by T. Rowe Price.5 Morgan Stanley estimates private credit could supply more than half of the $1.5 trillion needed for global data-center construction through 2028.6

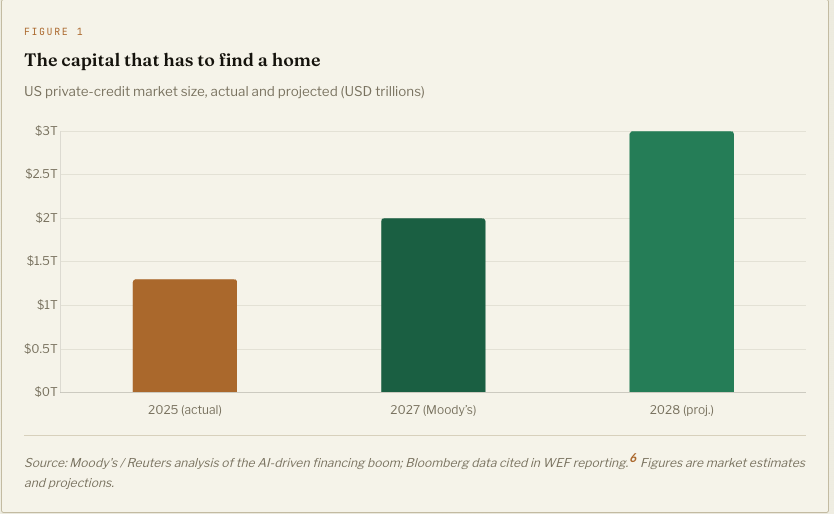

Private credit is scaling to meet that demand, but the absorption gap is real and growing. The asset class sits near $1.3 trillion today and is forecast to reach roughly $2 trillion by 2027 (Moody’s) and approach $3 trillion by 2028.6 Even at that pace, supply is racing to keep up with AI-accelerated origination across every credit vertical.

When intelligence scales faster than funding, the winner isn’t whoever has the best model — it’s whoever lined up demand for the output first.

02 / THE FIX

Why multiple off-take agreements are the only viable answer

When origination outpaces fundraising, there is one structurally sound response: secure committed demand for the output before you produce it. Forward flow is the cleanest expression of this — an institutional buyer pre-commits to purchase a defined volume of assets on agreed terms — but it sits inside a broader category of off-take agreements that move asset-absorption risk off the originator and onto the capital partner.

The strategic point is that these agreements must not be singular. A single forward-flow line is a lifeline; a diversified stack of off-take agreements is an operating system. Upstart’s resilience came precisely from layering counterparties — Fortress, Centerbridge, Eltura — across structures and durations, reducing single-partner concentration and letting the funding base grow in step with origination rather than lagging it.2

Positioned correctly, this architecture changes the growth math. Because committed demand expands alongside origination capacity, deal flow becomes structurally scalable — each new off-take line raises the ceiling on the volume a platform can profitably move, which lifts revenue throughput across the system. This is not a claim of unlimited returns; it is the more durable claim that the ceiling on deal flow becomes a function of committed capacity, and committed capacity can be added, repeatedly, by signing partners.

03 / THE PREMIUM

Why the market pays up for AI-layered credit

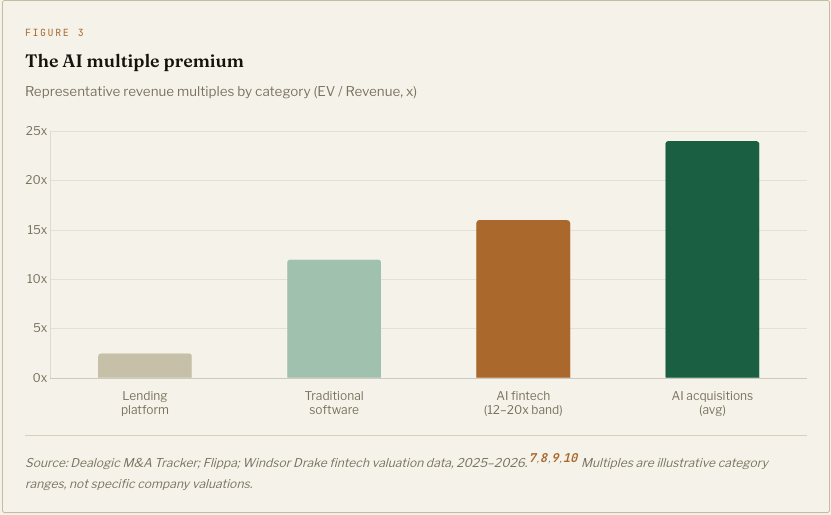

The exit data explains the urgency. Plain consumer-lending platforms trade at roughly 2.5x revenue, and the broad fintech median compressed to the mid-single digits through 2025.7 But AI changes the multiple. According to Dealogic’s M&A Tracker, AI acquisitions command average revenue multiples near 24x, versus about 12x for traditional software.8 Growth-stage AI businesses with clear traction transact in the 8x–20x range, and AI-enabled financial infrastructure reaches 10x-plus.9,10

That is the band a company sits in when it credibly layers fintech + AI + direct lending. The result is what AI fintechs exiting at 12x–20x revenue already demonstrate, and it is the band CR Equity AI is built to occupy.

04 / THE COMPANYCR Equity AI: the Kaizen credit layer in practice

CR Equity AI’s credit layer is built on a “Kaizen” model — continuous improvement as an operating ethos — designed to do three things in tandem: learn continuously from every loan and deal that flows through the system, de-risk investment opportunities through vetted, rigorous underwriting, and stay relentlessly ROI-focused on the outcomes that matter to capital partners.

The stack pairs integrated marketing that drives targeted investment toward qualified opportunities with automated AI underwriting, while maintaining security and transparency through AES-256 encryption and a blockchain settlement layer. Layering fintech, AI, and direct lending under a Kaizen ethos is what is generating a favorable investor outlook — in a market where AI fintechs are exiting at 12x–20x revenue.

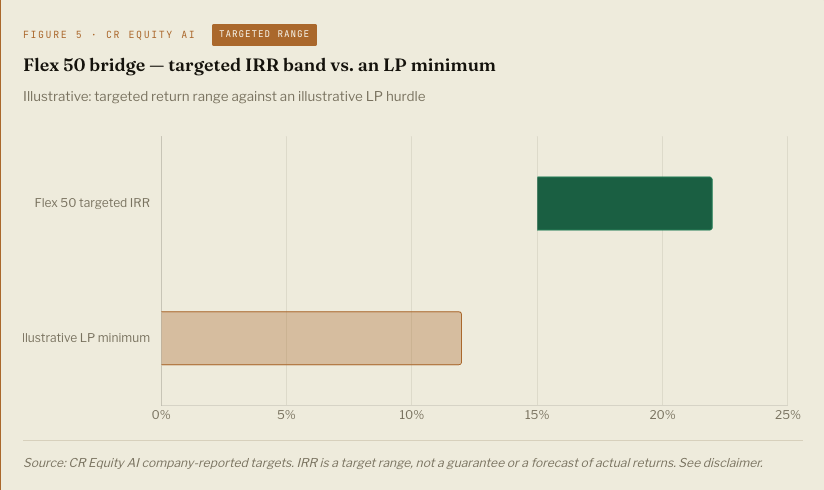

A case in point — May 24, 2026. CEO Rob Stewart met with prospective LP Onvestir, walked them through a live platform demo and the financials, and asked for their minimum IRR and target credit-box requirements. The alignment was nearly immediate: Stewart and CR Equity matched the firm’s parameters to the company’s signature product, the Flex 50 bridge — a structure targeting a purported 15%–22% IRR.

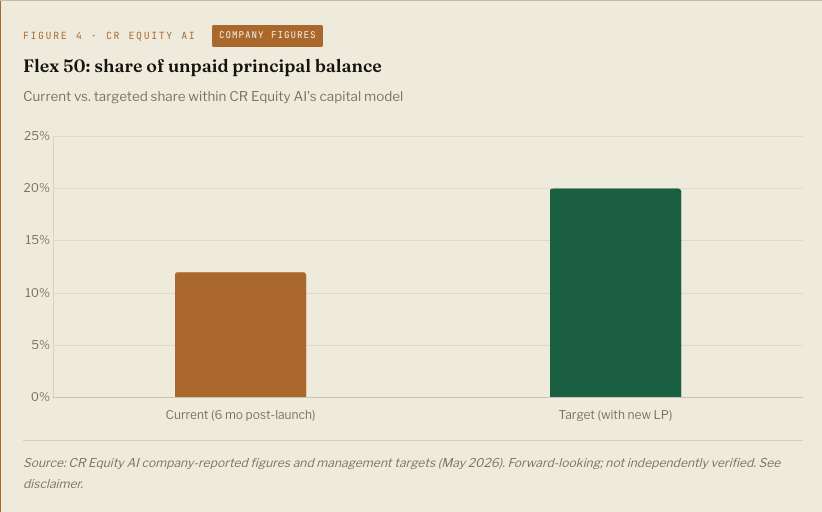

Flex 50 was unveiled to CR Equity’s client base in 2025 as a fast, emergent financing solution. Within six months it grew to command 12% of the company’s unpaid principal balance (UPB) inside its capital model. With the new LP partnership, CR Equity intends to grow Flex 50 from 12% to 20% of UPB — an expansion the company projects would lift revenue by roughly 8% on a cash-on-cash basis.

15–22% Flex 50 targeted IRR | 12% → 20% Targeted share of UPB | ~8% Projected revenue lift, cash-on-cash | 6 mo To reach 12% of UPB post-launch |

05 / THE OPPORTUNITY

What this means for investors

The last cycle priced AI models. The next will reward the companies that solved capital throughput — the ones who lined up committed demand for what their AI produces before the rest of the field recognized the bottleneck existed. Upstart’s $3.4 billion proved the playbook at public-company scale. CR Equity AI is executing the same architecture earlier in its trajectory, with a multi-agreement off-take strategy and a Kaizen credit layer built in from the start rather than retrofitted under pressure.

For investors, the entry point is the structural advantage itself: backing the funding architecture before the throughput it unlocks is fully reflected in valuation.

Investor Relations

See the platform, the underwriting, and the off-take model.

CR Equity AI is engaging qualified investors and capital partners. Request a platform demo and the full financials — including the Flex 50 structure and current off-take pipeline.

Sources & References

- Upstart Holdings, “Upstart Announces $1.25B Forward-Flow Agreement with Fortress Investment Group,” Business Wire, Apr. 29, 2026. ir.upstart.com

- Upstart forward-flow commitments (Fortress $1.25B, Centerbridge $1.2B, Eltura/Aperture $1.0B), as compiled in TIKR market analysis, May 26, 2026. tikr.com

- “Upstart Stock Has Fallen 67% From Its 52-Week High…,” TIKR, May 26, 2026 (Q1 2026 revenue +44% YoY to $308M). tikr.com

- S&P Global Ratings, “Private Credit, Tech Issuance fuelled by AI… Liquidity Outlook 2026,” Feb. 17, 2026 (top-five US hyperscaler capex ~$600B in 2026, +38%). press.spglobal.com

- T. Rowe Price, “How the new AI economy is reshaping global credit markets,” Mar. 2026 (Bloomberg Finance L.P. data; capital markets and debt to fund AI capex). troweprice.com

- Reuters analysis of the AI-driven data-center boom (Morgan Stanley: private credit could fund >50% of $1.5T buildout through 2028); Moody’s (~$2T by 2027); US private credit ~$1.3T, approaching ~$3T by 2028. via Creative Planning

- Windsor Drake, “Fintech Valuation Multiples,” Feb. 2026 (lending platforms ~2.5x revenue; AI-enabled infrastructure 10x+). windsordrake.com

- Dealogic M&A Tracker, as cited in AI startup funding statistics, 2026 (AI acquisitions ~24x revenue vs ~12x for traditional software). secondtalent.com

- Flippa, “AI Startups Valuation Multiples: Key Considerations for 2026” (growth-stage AI 8x–20x revenue). flippa.com

- FE International, “AI M&A Trends 2026: Why Acquirers Pay Premium Multiples,” Apr. 2026. feinternational.com

Disclaimer. This article is for informational purposes only and does not constitute investment, financial, legal, or tax advice, nor an offer to sell or a solicitation of an offer to buy any security. Figures attributed to CR Equity AI — including Flex 50 IRR targets, UPB share, projected revenue impact, and the described LP discussion — are company-reported and forward-looking; they are management estimates and targets, have not been independently verified, and are not guarantees of future performance or returns. Actual results may differ materially. Market data attributed to third parties reflects those sources as of the dates cited. Past performance and projected returns do not predict future results. Prospective investors should conduct independent due diligence and consult qualified advisors before making any decision.