7 min read

Tokenization of CRE equity gets the headlines — fractional shares of a trophy tower make for an easy story. The more consequential shift may be quieter and on the debt side, where tokenized notes and functioning secondary markets could finally bring liquidity to one of the most illiquid asset classes in finance.

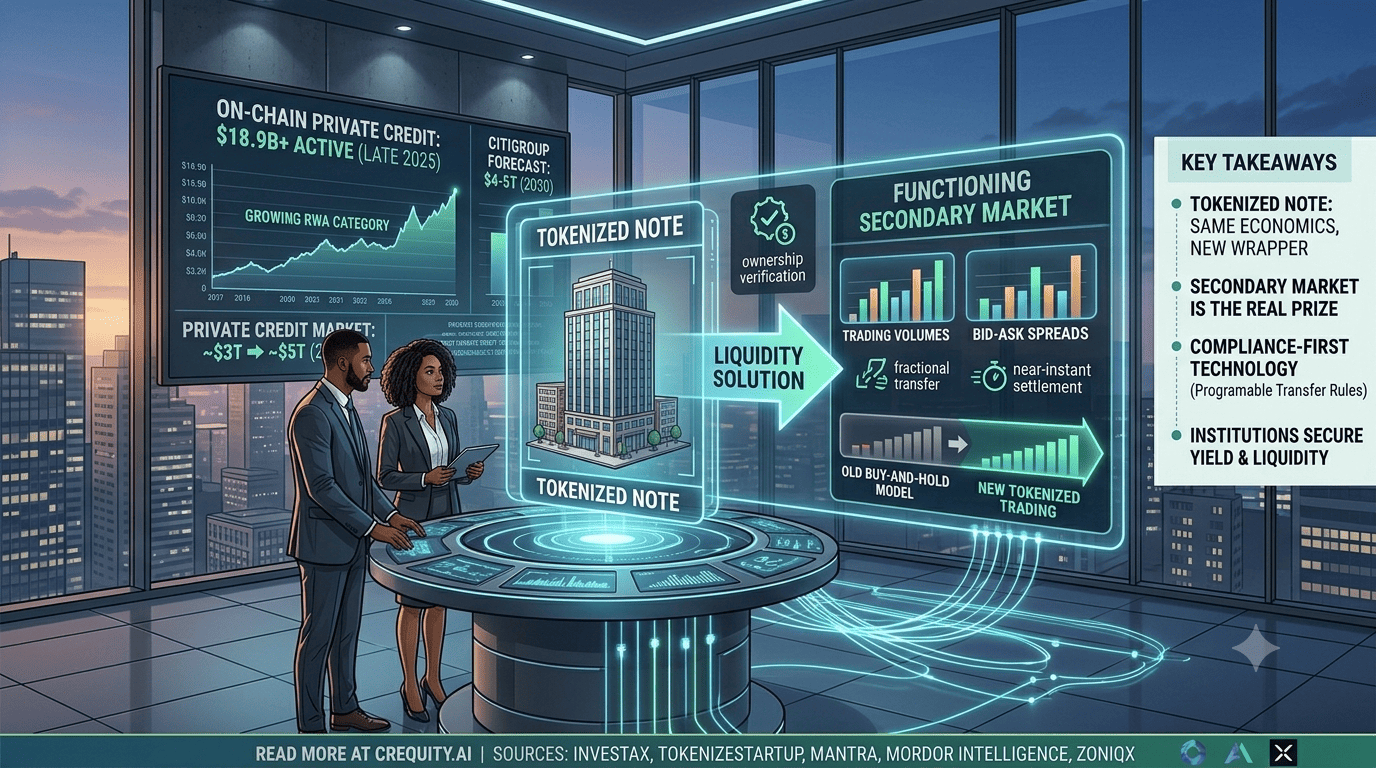

The momentum is no longer theoretical. Private credit is already the largest category of tokenized real-world assets: active on-chain private credit exceeded $18.9 billion in late 2025, with cumulative originations around $33.7 billion, according to industry tracker rwa.xyz. Forecasts for where tokenized securities go from here range widely — Citigroup projects $4–$5 trillion by 2030 — but the direction is not in dispute. Debt is moving on-chain.

What a tokenized note actually is

A tokenized note is a debt instrument — a loan, a participation, a tranche — represented as a digital token on a blockchain. Ownership, payment rights, and transfer history live on a shared ledger rather than in a stack of paper held by a single servicer.

The economics of the instrument do not change. A loan is still a loan; the cash flows are the same. What changes is how easily ownership can be verified, divided, and transferred — the exact mechanics that determine whether a secondary market can exist at all. That is the whole game: not a new kind of debt, but a new way of moving it.

Why secondary trading is the real prize

CRE debt has historically been a buy-and-hold proposition. Once a loan is originated, selling a participation means a bilateral negotiation, manual documentation, and a slow transfer process. That friction keeps capital locked up and suppresses the price discovery a liquid market provides — you cannot price what rarely trades.

Tokenized notes make fractional, near-instant transfer feasible. A lender can sell a portion of a position to rebalance risk; an investor can enter at a size that suits them rather than the size the deal happens to require. Early platforms are already building toward this — regulated trading venues have processed hundreds of millions in CRE tokenizations via private-placement structures and are targeting 24/7 secondary trading. When transfer becomes cheap and fast, liquidity changes how the entire asset class is priced and held.

The technology does not create a regulatory loophole

This is where discipline matters most, and where a lot of hype falls apart. Tokenized debt instruments are still securities. They live under existing securities law — exemptions, investor accreditation, disclosure obligations, and transfer restrictions all apply. The token wrapper does not create a regulatory gray zone; it has to operate inside the one that already exists.

The platforms that win here will treat compliance as the foundation, not the afterthought — building transfer restrictions and investor verification directly into the token logic rather than bolting them on later. Tellingly, compliance and legal-technology services are among the fastest-growing segments of the tokenization market, a sign that serious capital understands the constraint. Programmable compliance, where the rules travel with the asset, is the feature that makes institutional adoption possible at all.

Why institutions are paying attention

Institutional capital wants the yield of private credit without permanently surrendering liquidity — historically a contradiction, since the illiquidity was part of the yield. Tokenized debt and the secondary markets it enables offer a path to having both: hold the exposure, but keep the option to exit.

The structural backdrop makes the timing logical. Private credit grew to roughly $3 trillion entering 2025 and is projected to approach $5 trillion by 2029 as banks continue to retreat from segments of commercial lending. An asset class growing that fast eventually demands better infrastructure for moving risk around. Institutional investors already account for the large majority of tokenization activity — they are not watching from the sidelines.

Key takeaways

-

Tokenized private credit is already the biggest RWA category — $18.9B active on-chain, ~$33.7B cumulative originations (rwa.xyz, late 2025).

-

A tokenized note keeps a loan’s economics identical but makes ownership easy to verify, divide, and transfer.

-

Secondary-market liquidity — not the token itself — is the real prize, enabling price discovery in a buy-and-hold asset class.

-

Tokenized debt is still a security; the winning platforms build accreditation and transfer rules into the token rather than bolting compliance on later.

-

With private credit heading toward ~$5T by 2029, institutions want yield without permanently giving up liquidity — exactly what tokenization offers.

The infrastructure for tokenized CRE debt is early, but the direction is set and the capital is institutional. The platforms that matter will be the ones that pair liquidity with compliance from the first line of code. To see how CR Equity AI connects underwritten, compliant assets to capital on one intelligence layer, request a walkthrough at crequity.ai or contact the team at support@crequity.ai.

Sources

-

InvestaX — What Is Real-World Asset (RWA) Tokenization? A Full Guide for 2026 (private credit on-chain figures) — https://investax.io/blog/what-is-real-world-asset-rwa-tokenization

-

TokenizeStartup — Tokenization Market Size Projections (Citigroup 2030 forecast) — https://tokenizestartup.com/analysis/tokenization-market-size/

-

MANTRA — The Tokenization of Private Credit (private credit market size) — https://mantrachain.io/resources/announcements/the-tokenization-of-private-credit

-

Mordor Intelligence — Asset Tokenization Market (segment growth, compliance-tech) — https://www.mordorintelligence.com/industry-reports/asset-tokenization-market

-

Zoniqx — Top Real Estate Tokenization Platforms 2025 and 2026 (secondary trading venues) — https://www.zoniqx.com/resources/top-real-estate-tokenization-platforms-in-2025-and-2026