Why Transparency in Commercial Lending Matters Now

Commercial lending has long carried a reputation for opacity. Borrowers submit applications, documents disappear into underwriting, and weeks later an approval or denial arrives with little explanation. That experience is not inevitable. Transparency in commercial lending improves risk assessment by providing clear visibility into borrower financials, assets, and repayment capacity, leading to more accurate underwriting decisions. For real estate investors and small business owners, understanding how transparent lending works, and demanding it, is no longer optional. It is a direct advantage in securing faster approvals, better terms, and fewer costly surprises.

Table of Contents

- What transparency actually means in commercial lending

- Five key ways transparency de-risks and accelerates financing

- Transparency mechanisms: How lenders build trust and compliance

- Risks of non-transparency: Hidden costs and real-world headaches

- When transparency matters most: Edge cases and market trends

- Our perspective: Why true transparency is non-negotiable in 2026 and beyond

- How CR Equity AI makes commercial lending transparent and efficient

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Clarity reduces risk | Transparent lending helps investors and businesses avoid costly misunderstandings and defaults. |

| Faster, fairer decisions | Clear criteria and open communication speed up approvals and reduce delays. |

| Watch for hidden fees | Opaque lending practices often hide extra costs that can surprise or harm borrowers. |

| Regulations are evolving | Staying updated on compliance helps you pick lenders who are committed to transparency. |

| Transparency is a competitive advantage | Demanding insight into your financing terms is key to long-term business success. |

What transparency actually means in commercial lending

Now that you see why the default process feels confusing, let’s define what true transparency means in practice.

In commercial lending, transparency is not simply about disclosing a rate sheet. It refers to a consistent, structured practice of open communication between borrower and lender at every stage of the credit lifecycle. It means your application requirements are stated upfront, your underwriting criteria are reviewable, your fees are itemized, and your loan monitoring is an ongoing two-way process rather than a one-sided reporting obligation.

Practically speaking, transparent lending involves four core elements:

- Clear disclosures: All fees, conditions, and rate structures are presented before commitment, not buried in closing documents.

- Reviewable criteria: Borrowers can access the data points and financial ratios that determine creditworthiness, including debt service coverage ratio (DSCR), loan-to-value (LTV), and net operating income (NOI) thresholds.

- Traceable workflows: Every step of the underwriting process is documented and can be audited by both parties, reducing disputes later.

- Explainable AI: Where machine-learning models assist in credit decisioning, the logic behind scores and recommendations is communicated in plain terms, not reduced to a pass/fail output. Platforms using AI-driven underwriting in commercial real estate are raising the bar for this type of explainability.

Transparency also extends into ongoing loan monitoring. Once funding closes, a transparent lender continues to provide structured reporting on covenant compliance, rate adjustments, and portfolio health. This reduces the risk of surprises at renewal or when market conditions shift.

Pro Tip: Before signing a term sheet, ask your lender for their underwriting criteria in writing and request a sample term sheet from a comparable recently closed deal. A lender that hesitates to provide either is signaling opacity.

Five key ways transparency de-risks and accelerates financing

With a clearer view of what transparency is, let’s break down exactly how it creates real-world value for your next financing deal.

Financial transparency reduces default risks and operational inefficiencies by minimizing misunderstandings, ensuring consistent data for projections, and fostering accountability across all parties in the lending relationship. That is not an abstract principle. It has measurable, deal-level consequences.

Here are five concrete ways transparent lending delivers value:

-

Reduced default risk. When borrowers fully understand their repayment obligations, covenant structures, and trigger events, they are better positioned to manage cash flow proactively. Lenders who require detailed, verified financial data upfront are simultaneously protecting their own portfolios and helping borrowers avoid overleveraging.

-

Faster time to funding. Opaque processes generate back-and-forth document requests, stalled approvals, and last-minute condition clears. Transparent platforms that publish checklist requirements and use automated document verification can reduce approval timelines from weeks to days. Reviewing AI lending examples shows how structured data flows are eliminating the friction that historically inflated commercial loan timelines.

-

Fewer closing disputes. Hidden fees and ambiguous rate adjustments are a primary source of deal fallout. When a borrower reviews a transparent fee worksheet at application, there are no surprises at the closing table. This protects deal momentum and preserves lender-borrower relationships.

-

Better loan terms through trust. Lenders extend better pricing and structure to borrowers who present clean, complete, and verifiable financials. When a borrower’s documentation is transparent and the lender’s criteria are equally clear, negotiations become more efficient and outcomes tend to favor borrowers with strong underlying fundamentals.

-

Streamlined underwriting review. Understanding the specific underwriting steps in commercial real estate allows borrowers to pre-structure their submissions to match lender requirements, which accelerates committee review and reduces conditions.

“Transparency is not a courtesy offered by lenders. It is a structural efficiency that benefits both sides of the capital table. When borrowers and lenders operate with consistent data and clear criteria, the credit market functions at a higher level.”

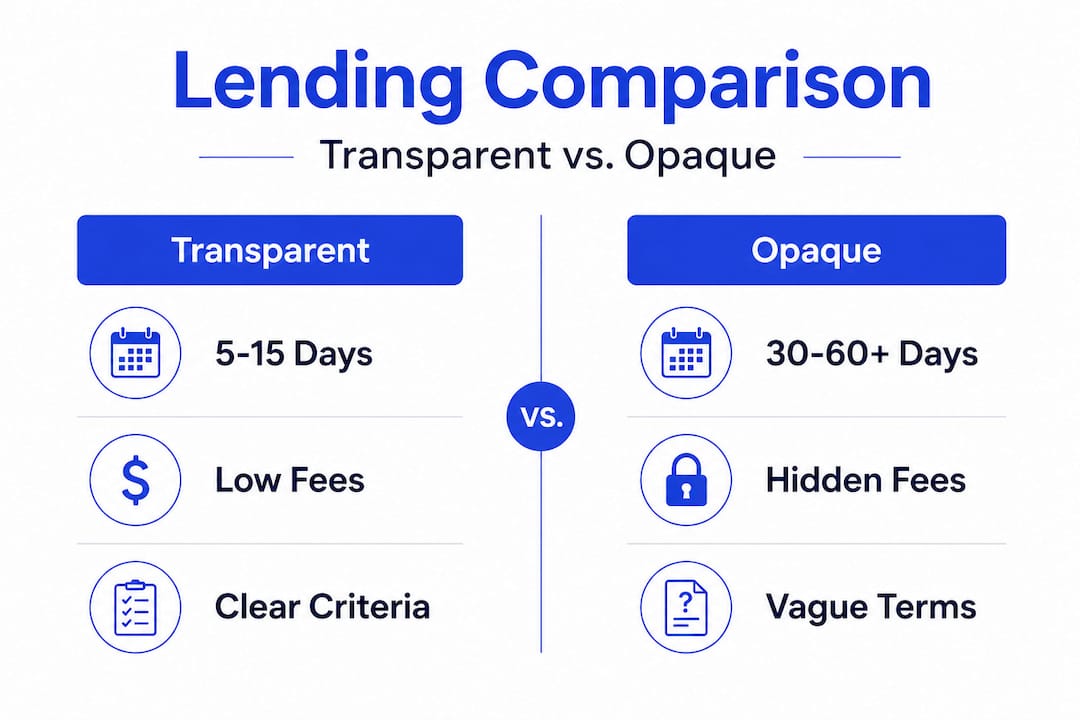

The following table illustrates the direct performance difference between transparent and opaque lending processes:

| Factor | Transparent lending | Opaque lending |

|---|---|---|

| Time to funding | 5 to 15 business days | 30 to 60+ business days |

| Default risk | Lower, due to verified data | Higher, due to misaligned expectations |

| Borrower satisfaction | High, clear terms and milestones | Low, frequent surprises and delays |

| Dispute frequency | Minimal | Elevated, especially at closing |

| Rate accuracy | Locked early in process | Subject to last-minute adjustments |

Transparency mechanisms: How lenders build trust and compliance

Knowing the advantages, let’s see what steps lenders actually take to build and demonstrate transparency.

Transparency involves structured disclosures, clear criteria, explainable AI for underwriting, and traceable data lineage, all of which streamline evaluations for property acquisitions and operations. Lenders who implement these mechanisms demonstrate compliance readiness and institutional reliability. Here is how those mechanisms operate in practice:

- Structured fee disclosures: Origination fees, legal costs, appraisal charges, prepayment penalties, and exit fees are all itemized and delivered at term sheet stage. This practice aligns with OCC regulatory guidance that emphasizes clear communication of loan costs and conditions.

- Document checklists: Lenders publish standardized lists of required items, organized by loan type, including tax returns, rent rolls, operating statements, entity documentation, and environmental reports. Borrowers know exactly what is needed before the first submission.

- Explainable AI in credit decisioning: Advanced underwriting platforms now provide scoring rationale alongside credit decisions. Rather than a single approval or denial output, borrowers receive a breakdown of which factors most influenced the decision and what thresholds were applied. Reviewing how the AI underwriting process works clarifies how these explainability features are integrated into modern platforms.

- Ongoing monitoring and reporting: Post-closing, transparent lenders provide borrowers with regular performance reports, covenant compliance dashboards, and advance notice of rate resets or maturity events.

The following table summarizes key transparency mechanisms and their direct benefit to borrowers:

| Mechanism | How it works | Benefit to borrower |

|---|---|---|

| Structured fee disclosure | Itemized costs delivered at term sheet | No closing surprises |

| Document checklist | Standardized, loan-type specific | Faster, cleaner submissions |

| Explainable AI scoring | Decision rationale provided in plain language | Understand approval or denial basis |

| Covenant monitoring dashboard | Real-time compliance tracking | Proactive default prevention |

| Rate reset notifications | Advance written notice of changes | Budget and planning accuracy |

These mechanisms are not merely best practices. They are increasingly codified through federal and state regulatory frameworks that hold lenders accountable for disclosure quality and consistency.

Risks of non-transparency: Hidden costs and real-world headaches

It is just as important to know the danger zones. Here is what can go wrong when transparency is missing.

Opaque lending practices, including black-box AI models and hidden fees in nonbank lending, can lead to higher effective borrowing rates and disputes for small businesses. These outcomes are not edge cases. They appear regularly in commercial transactions where either the lender lacks disclosure infrastructure or the borrower fails to demand it.

The most common risk categories in non-transparent lending include:

- Black-box decisioning: When AI or algorithmic models determine credit outcomes without disclosing evaluation criteria, borrowers cannot correct inaccurate data, challenge unfair assessments, or understand how to improve their profile for reapplication. This is particularly damaging for real estate investors whose portfolios include non-standard assets or unconventional income streams.

- Hidden charges at closing: Balloon fees, undisclosed origination points, rate floor adjustments, and administrative costs that appear only in the final closing disclosure represent some of the most common sources of transaction fallout. Even a half-point fee on a $5 million commercial mortgage represents a $25,000 surprise that borrowers did not budget for.

- Inadequate loan servicing communication: Opaque monitoring practices mean borrowers may not receive timely notice of covenant breaches, escrow shortfalls, or maturity extensions. This creates default risk through administrative failure rather than underlying financial distress. The risks of hidden fees in commercial appraisals represent one concrete category of these disclosure gaps.

- Rate ambiguity in floating-rate structures: Without transparent reset schedules and margin calculation methods, borrowers in variable-rate commercial loans may face payment adjustments they did not anticipate or have contractual grounds to challenge.

Pro Tip: Always request a complete fee worksheet before committing to any commercial loan. This document should itemize every cost you will pay from application through closing, including third-party expenses the lender controls or requires.

When transparency matters most: Edge cases and market trends

But when does transparency matter most? Here are critical situations and industry shifts you need on your radar.

In venture lending and early-stage business financing, transparency in projections and monitoring is critical due to high failure risk. The OCC has placed renewed emphasis on prudent underwriting standards and granular risk-rating practices, particularly for lenders serving emerging companies and non-stabilized commercial properties. When cash flow is not yet established, the quality of forward-looking financial data and the lender’s ability to explain how those projections are evaluated become the primary basis for credit decisions.

Three specific scenarios where transparency is most critical:

-

Venture and startup lending: Companies without multi-year operating history depend on transparent projection modeling to demonstrate repayment capacity. When lenders do not disclose how they evaluate those projections, borrowers cannot optimize their presentations or identify gaps before underwriting.

-

Collateral-free loan programs: Mandating collateral-free lending without transparency infrastructure may increase systemic risks and reduce credit supply, as collateral traditionally serves as a risk signal in information-asymmetric markets. Without collateral, the quality and clarity of financial disclosures become the primary risk mitigation tool. Transparency fills the gap that collateral once occupied.

-

Bridge and construction financing: These loan structures carry higher execution risk than permanent financing. Draw schedules, completion guarantees, and interest reserve calculations must all be disclosed and explained clearly to prevent cost overruns from compounding into default.

Regulatory pressure is accelerating these requirements across the industry. The future of AI-powered business lending increasingly involves real-time audit trails and explainable scoring as baseline compliance expectations, not optional features. Reviewing regulatory compliance standards for lender transparency illustrates how disclosure requirements are tightening at the state level as well.

Pro Tip: When evaluating lenders for early-stage or collateral-light programs, look specifically for those that provide scenario-based projections showing how your loan performs under stress conditions, not just base-case assumptions.

Our perspective: Why true transparency is non-negotiable in 2026 and beyond

Here is an uncomfortable truth about commercial lending: many borrowers chase the lowest rate and walk away from the most important variable, which is information. They accept opaque term sheets, skip the fee worksheet review, and discover at closing that their effective cost of capital is materially higher than the headline number suggested. This is not rare. It is common enough to be a pattern.

The conventional wisdom says to compare rates across lenders and choose accordingly. Our position is that rate comparison without transparency comparison is incomplete analysis. A lender offering 25 basis points less than competitors, but operating with black-box underwriting, undisclosed reserve requirements, and inconsistent servicing communication, will cost you more over the life of the loan than that rate differential will save.

The rise of AI decisioning has made this more urgent, not less. As more lenders deploy machine-learning models for credit scoring, the risk of unexplained decisions is increasing. Explainability is not a feature to appreciate. It is a compliance expectation and a borrower right. Engaged investors are increasingly demanding audit trails and real-time portfolio updates as a condition of capital deployment, not as a preference.

Here is the contrarian view: in a market where instant decisioning is becoming standard, your ability to demand, interpret, and act on transparent credit information is a genuine competitive edge. Borrowers who understand their own credit profile, who require explainable underwriting, and who verify fee structures before commitment consistently secure better terms than those who simply accept the first offer. Real-time lender matching for greater transparency is one practical application of this principle, allowing borrowers to compare multiple lender positions with full fee visibility before committing.

Transparency is not softness. It is precision. And in commercial real estate and business finance, precision wins.

How CR Equity AI makes commercial lending transparent and efficient

Ready to put transparency into practice? Here is how CR Equity AI can help you take the next step with clarity and confidence.

CR Equity AI is built around the principle that borrowers deserve to see exactly how their credit is being evaluated and exactly what their financing will cost. The platform delivers real-time quotes with itemized terms, explainable AI credit scoring, and automated document verification that eliminates the back-and-forth that delays traditional commercial loans.

Whether you are acquiring a self-storage facility, refinancing a mixed-use property, or seeking working capital for your business, CR Equity AI’s CRE business financing services provide structured, compliant loan programs with full fee disclosure from the first interaction. You can begin by generating an instant loan quote that shows rate ranges, eligible products, and estimated costs in minutes, not weeks. CR Equity AI brings institutional-grade underwriting standards and transparent credit infrastructure to real estate investors and business owners who need speed without surprises.

Frequently asked questions

How does transparency improve commercial loan approvals?

Transparency improves risk assessment by giving lenders clear visibility into borrower financials, assets, and repayment capacity, which results in more accurate underwriting decisions and higher approval confidence. When complete data is available, lenders can price risk more precisely and structure loans that borrowers can successfully service.

What are the biggest red flags if lending isn’t transparent?

Hidden fees, vague underwriting criteria, and unexplained loan denials are the most common warning signs of a non-transparent process. Opaque nonbank lending practices frequently result in higher effective borrowing costs and elevated dispute rates for small business borrowers.

Does AI help or hurt transparency in lending?

AI improves transparency when the models are explainable and criteria are disclosed, but black-box AI systems reduce borrower trust and increase the risk of unfair or unappealable credit decisions. The key distinction is whether the lender can explain why a model reached a specific conclusion in plain, reviewable terms.

Why is transparency especially important for startups or collateral-free loans?

Without collateral as a risk buffer, collateral-free lending without transparency infrastructure increases systemic risk and may reduce the availability of credit overall. Transparent projection modeling and clear underwriting criteria become the primary tools for establishing repayment credibility in the absence of pledged assets.

Recommended

- The Future of Business Lending Is Here — And It’s Powered by AI | CR Equity AI

- Blog | CR Equity AI

- AML & KYC for Digital Asset Lenders: What Institutions Need to Know | CR Equity AI

- The Non-QM Lending Opportunity: Credit Markets Beyond the GSE Box | CR Equity AI

- NJ lender appraisal guide: compliance and costs in 2026

- Build a financial due diligence checklist for smarter deals | Ready Accounting